Republican Senate Leadership on IMF Special Drawing Rights (SDRs): A Fact-Check

What are SDRs?

The COVID-19 pandemic has led to a variety of efforts to ensure that low- and middle-income countries have access to sufficient resources to import necessities like food, medicine, and personal protective equipment. One of those efforts involves an issuance of Special Drawing Rights, or SDRs, to the 190 member countries of the International Monetary Fund (IMF).

SDRs are a reserve asset issued by the IMF to its member countries. SDRs have a value that is based on a basket of five major currencies. Governments can exchange SDRs that they are holding for hard currencies, most often the dollar or euro, although the requesting government has to show need in order to do this. The other party to the exchange, who supplies the hard currency, is a government that has a surplus of hard currency reserves and volunteers to make the exchange.

The main advantage of using a new issuance of SDRs during the pandemic, in order to help individual countries in need, as well as to stabilize the world economy, is that the process is simple and can be relatively quick. An IMF issuance of SDRs does not cost the United States — or any IMF member country — anything. These reserve assets are not loans that have to be repaid, and therefore do not affect the sustainability of member countries’ public debt. Nor do they have conditionality attached to them.

For more information about SDRs and their role in addressing the effects of the pandemic, visit globalcovidresponse.org.

Fact-Checking GOP Senators' Claims

The Trump administration did not support a new issuance of SDRs when proposed by the IMF Managing Director in March 2020. Because the United States holds veto power at the IMF on votes regarding SDR issuances, the IMF was unable to issue SDRs despite nearly unanimous support from all other member countries. Under the Biden administration, the Treasury Department reversed course and recently announced that it will support an issuance of SDRs worth $650 billion. The amount falls short of the legislation supporting a 2 trillion SDR allocation that passed the US House twice last year, and that has been reintroduced in both the House and Senate this year. But it is a good first step for providing relief for low- and middle-income countries, and the amount is close to the most that the US Treasury Department can legally vote for at the IMF without getting prior approval from Congress for a greater amount.

Despite the fact that SDRs were successfully issued and used during the world recession of 2009, they are still not a well-known policy tool among US legislators. This can lead to misconceptions regarding the nature of SDRs, how they are used, and what countries they can help.

Case in point: the following letter from Republican Senators Pat Toomey (R-PA), Jim Risch (R-ID), John Kennedy (R-LA), and Bill Hagerty (R-TN) to Treasury Secretary Janet Yellen, strongly opposing a new issuance of SDRs, is filled with misconceptions and inaccurate information about SDRs.

The following is a fact-check of the March 24, 2021 letter from the Republican senators.

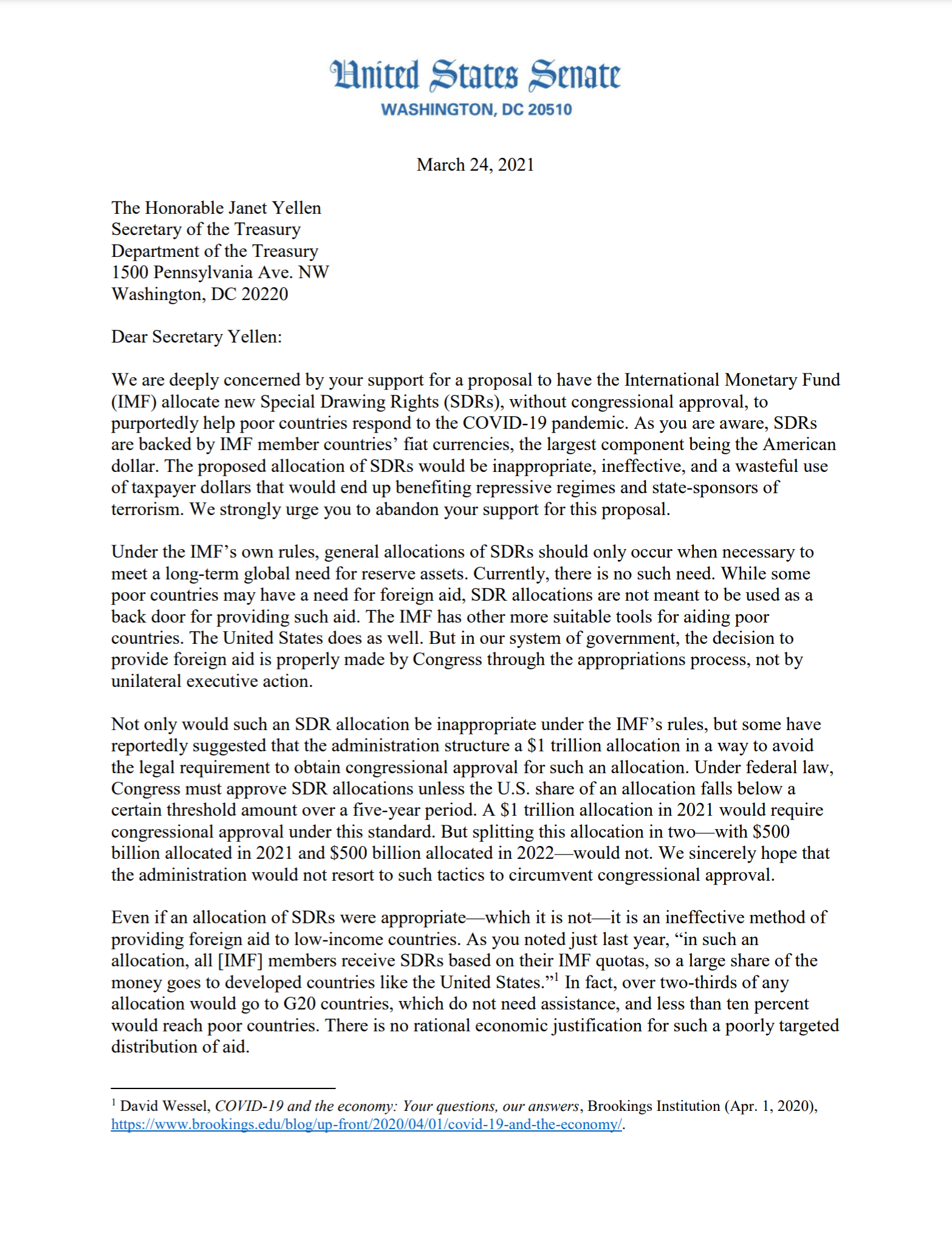

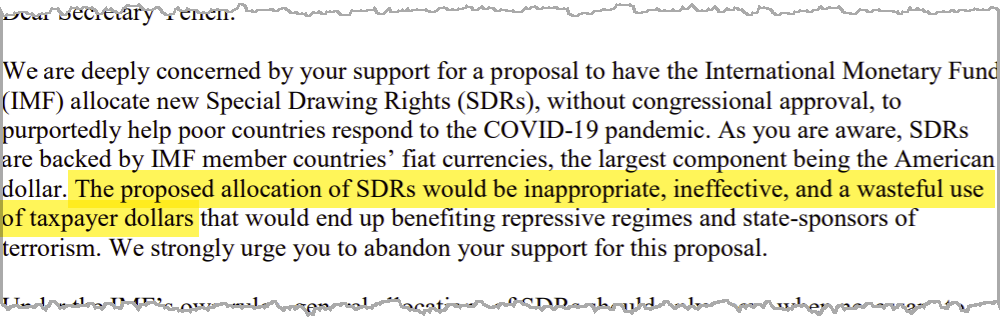

March 24, 2021 letter from Sens. Toomey, Risch, Kennedy, and Hagerty to Treasury Secretary Yellen regarding a new issuance of SDRs. (Click to read the full letter.)

March 24, 2021 letter from Sens. Toomey, Risch, Kennedy, and Hagerty to Treasury Secretary Yellen regarding a new issuance of SDRs. (Click to read the full letter.)

Claim 1:

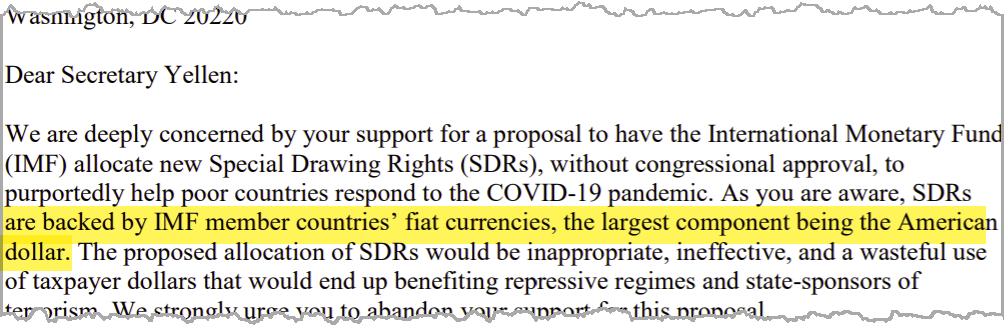

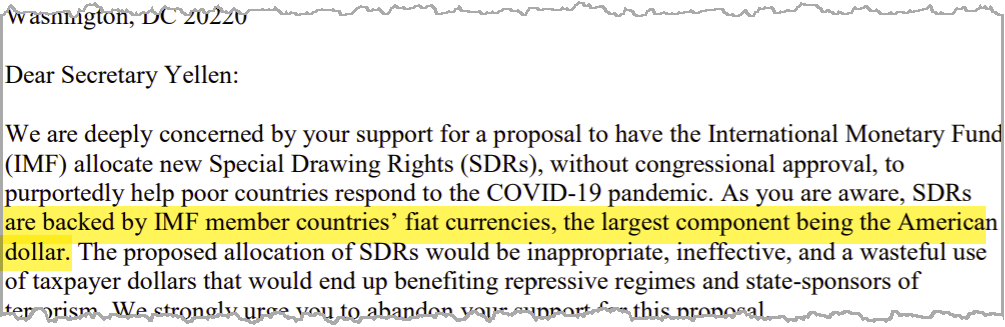

"...SDRs are backed by IMF member countries’ fiat currencies, the largest component being the American dollar."

Reality:

This implies that the US is somehow responsible for providing dollars in exchange for SDRs held by member countries, which is not true.

Claim 2:

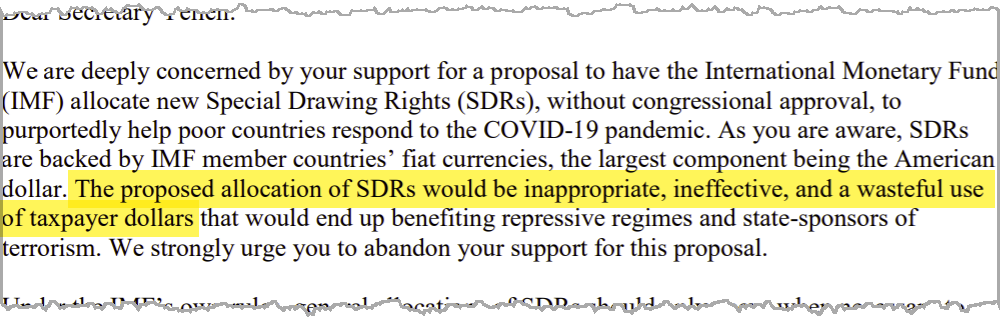

"The proposed allocation of SDRs would be...a wasteful use of taxpayer dollars..."

Reality:

This is false.

The phrase "wasteful use of taxpayer dollars" cannot be true about any SDR allocation. There are no US taxpayer dollars involved in the issuance or allocation of SDRs. Nor does the issuance or allocation of SDRs require the US government to provide dollars in exchange for SDRs.

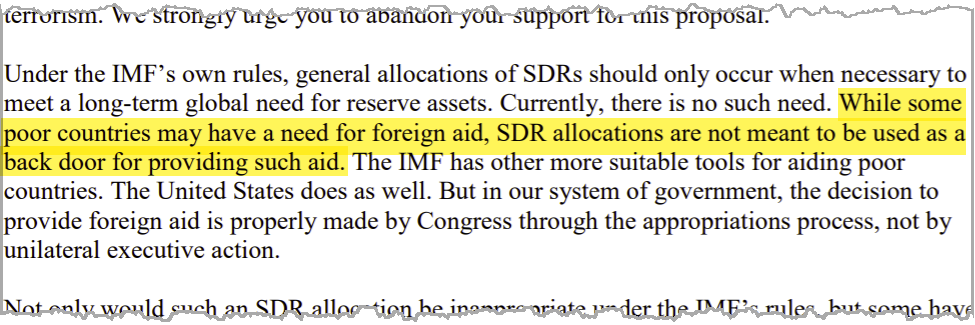

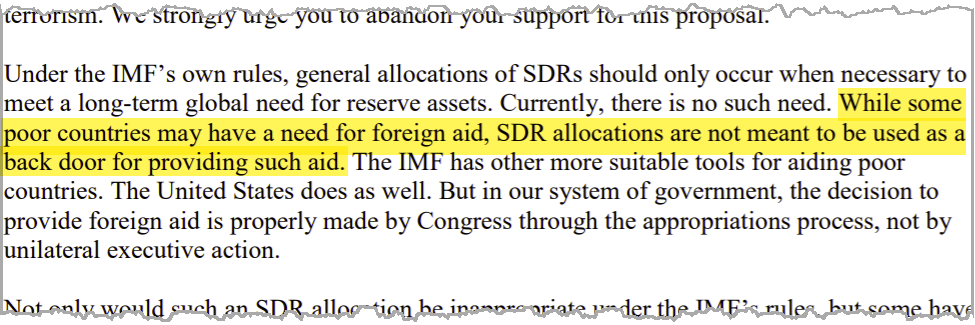

Claim 3:

"While some poor countries may have a need for foreign aid, SDR allocations are not meant to be used as a back door for providing such aid."

Reality:

SDRs are not foreign aid; an issuance of SDRs costs the US government nothing.

As the IMF has noted:

“[a]n SDR allocation is cost free. Allocating SDRs does not require contributions from donor countries’ budgets. SDRs are a reserve asset, not foreign aid. Most importantly, an SDR allocation does not add to any country’s public debt burden.”

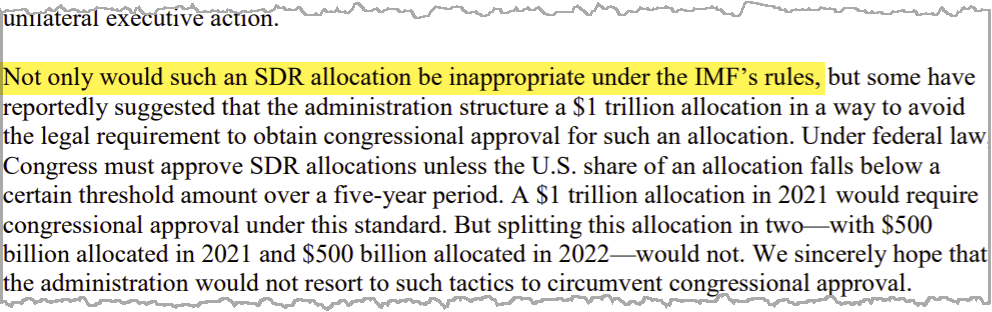

Claim 4:

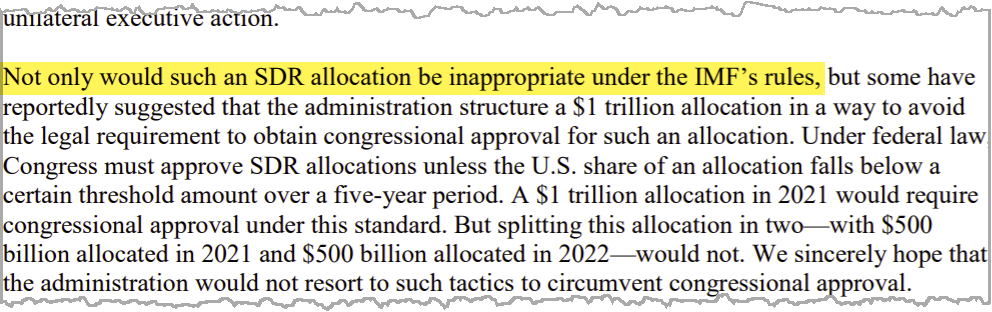

"Not only would such an SDR allocation be inappropriate under the IMF’s rules..."

Reality:

There is nothing inappropriate about this allocation under IMF rules.

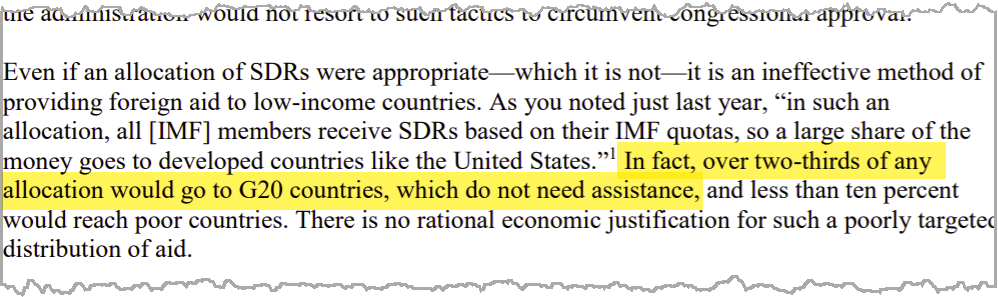

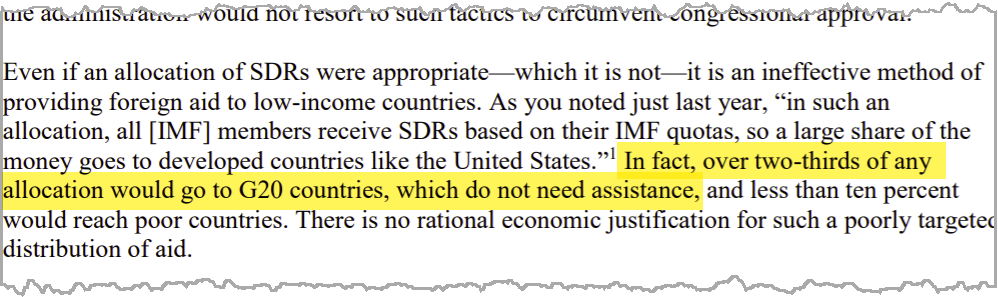

Claim 5:

"In fact, over two-thirds of any allocation would go to G20 countries, which do not need assistance..."

Reality:

This is true but none of the high-income countries would be able to convert the SDRs to hard currency because they cannot show need, as required. These SDRs would only be an accounting entry at the IMF, and not involve any use of real resources.

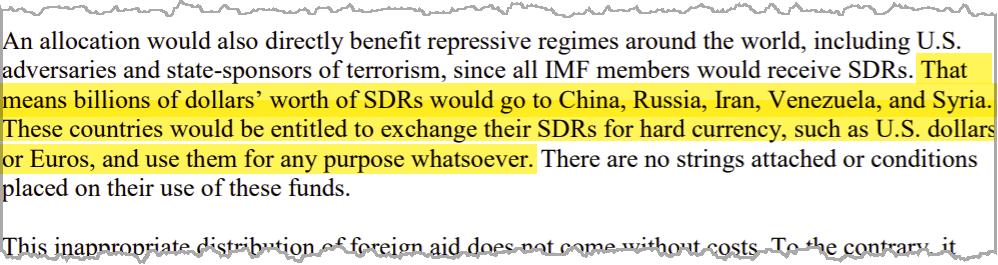

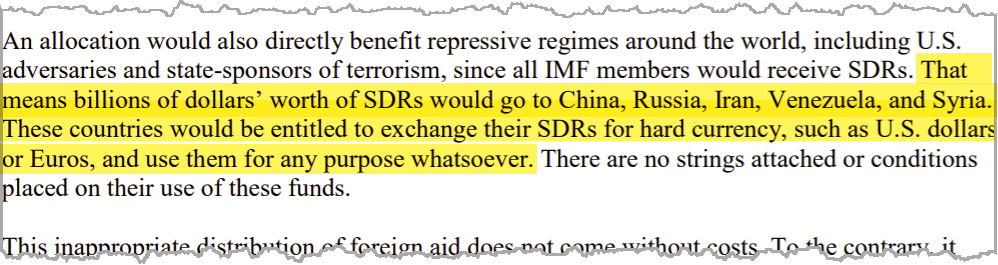

Claim 6:

"That means billions of dollars’ worth of SDRs would go to China, Russia, Iran, Venezuela, and Syria. These countries would be entitled to exchange their SDRs for hard currency, such as US dollars or Euros, and use them for any purpose whatsoever."

Reality:

China would not be able to convert SDRs to hard currency because it could not show need. It has more than $3 trillion in international reserves.

Furthermore, in 2015 China’s own currency became eligible to be added to the basket of currencies used to determine the value of the SDR; this is another reason that it would not be able to show need.

Iran would not be able to convert SDRs to hard currency because of US sanctions, and Venezuela would not be able to convert SDRs to hard currency for the same reason. Also, according to the IMF on April 16, Venezuela would be cut off from all SDRs “until a government is recognized” by the IMF.

Claim 7:

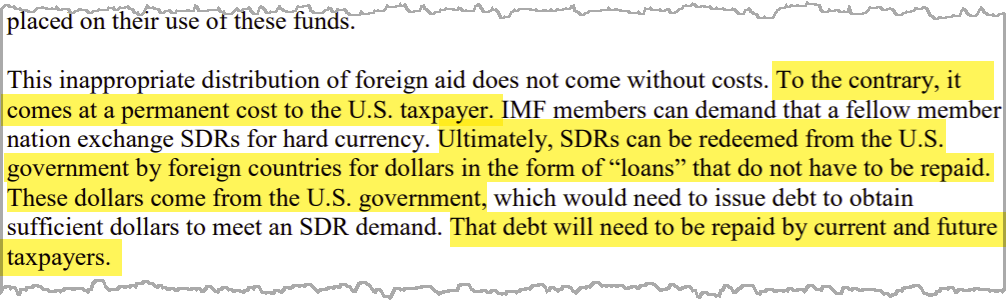

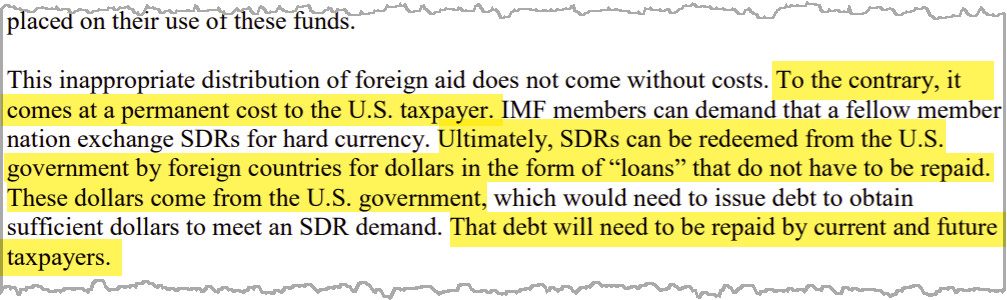

"To the contrary, it comes at a permanent cost to the US taxpayer. IMF members can demand that a fellow member nation exchange SDRs for hard currency. Ultimately, SDRs can be redeemed from the US government by foreign countries for dollars in the form of 'loans' that do not have to be repaid. These dollars come from the US government, which would need to issue debt to obtain sufficient dollars to meet an SDR demand. That debt will need to be repaid by current and future taxpayers."

Reality:

Again, the issuance of SDRs has zero cost to the US government. There will be no debt for current or future taxpayers.

And “SDRs can be redeemed from the US government by foreign countries for dollars” only if the US government chooses to do so. Most IMF members have dollars and other hard currencies that they can exchange for SDRs with countries in need (and many did so, in 2009 after the last special issuance of hundreds of billions of dollars worth of SDRs). Also, it is worth noting that less than 2 percent of the SDRs issued in 2009, during the world recession, were exchanged for hard currency.

***

The Center for Economic and Policy Research (CEPR) was established in 1999 to promote democratic debate on the most important economic and social issues that affect people’s lives. In order for citizens to effectively exercise their voices in a democracy, they should be informed about the problems and choices that they face. CEPR is committed to presenting issues in an accurate and understandable manner, so that the public is better prepared to choose among the various policy options.

If you appreciated this work, please consider supporting us with a donation.