Private Equity Tries to Protect Another Profit Center

Congress must step in to protect insured patients from unfair and unexpected medical charges.

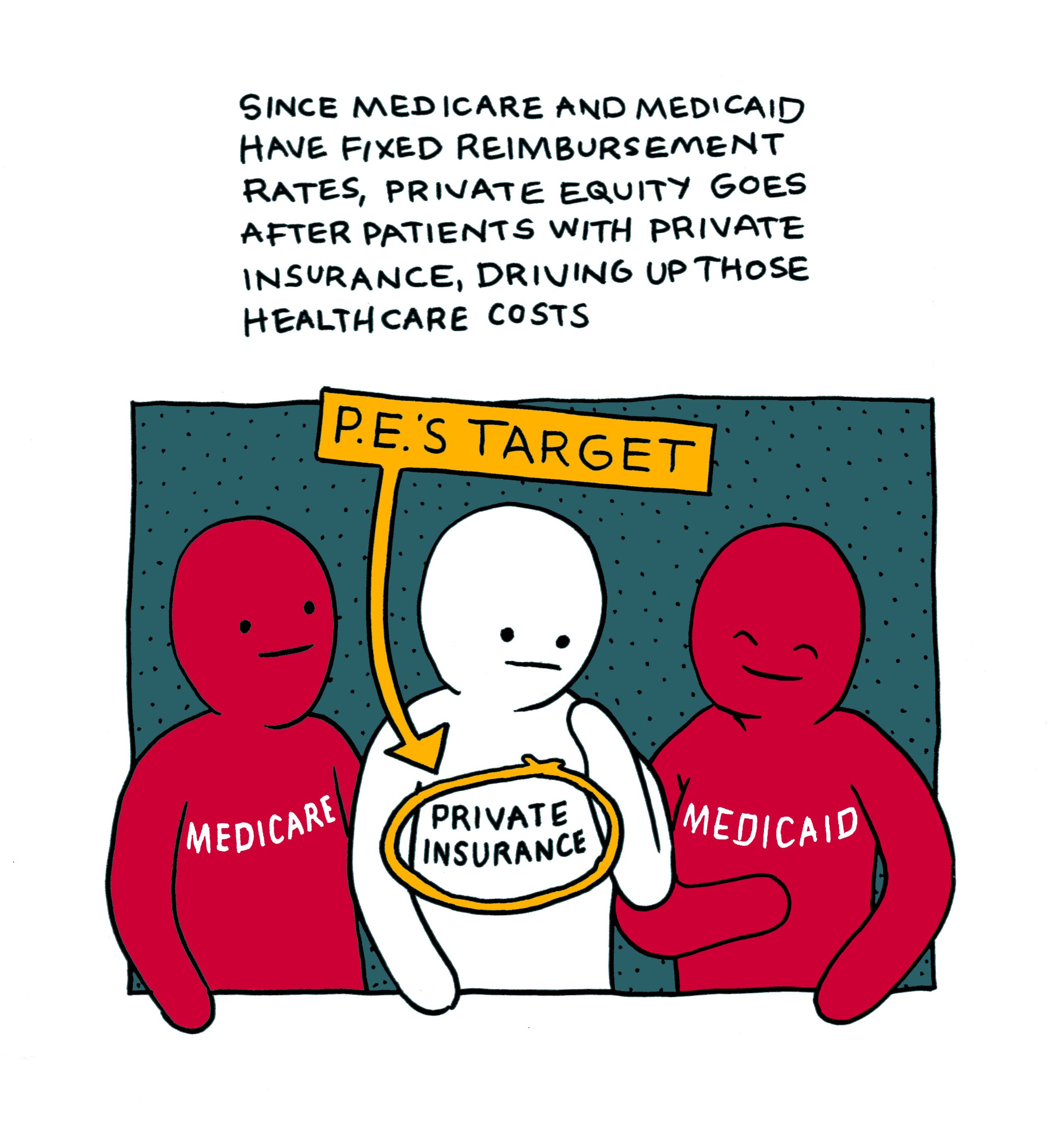

The fight in Congress heats up over surprise medical billing, another abuse of the public driven by the private equity industry. Medicare for All is poised to be the solution to this new "business."

Surprise medical billing has quickly become a small but critical flashpoint in health care reform. Because doctors and hospitals negotiate separately with insurance companies over reimbursement rates, it’s possible for a patient’s insurance to cover hospital charges while failing to cover the fees of some doctors in the hospital who are “out of network.” Patients who visit an emergency room (ER) or are admitted to an in-network hospital by an in-network doctor may find that some of the professionals who treat them are not covered by their insurance. That is because hospitals have outsourced ER, anesthesiology, radiology, or other specialized services to outside physician practices or staffing firms. Patients often find themselves on the hook for thousands, or even tens of thousands of dollars in surprise medical bills.

Twenty-five states have passed laws with limited protection for patients from out-of-network bills, usually for emergency room or urgent-care services; 20 more states are considering legislation. But these laws do not cover self-insured employer plans, which can only be regulated by the federal government. These plans cover an estimated 61 percent of workers who have private insurance, up from 44 percent 20 years ago. That means Congress must step in to protect insured patients from unfair and unexpected medical charges.

And that puts lawmakers up against the powerful and influential private equity industry, which plays a major role in supplying hospitals with physicians. They have aggressively bought up large national staffing firms or “physician practice management” (PPM) companies, as well as emergency providers that hospitals and other health organizations have outsourced, such as ground and air ambulance companies. And they are using the typical tools to protect their investments from a legislative onslaught: lobbying cash, dark-money front groups, and allies in Congress pushing loopholes and half measures.

The Role of Private Equity: Driving Market Concentration

Private equity funds use substantial debt to acquire doctors’ practices through leveraged buyouts, and to finance mergers of practices into large staffing firms. Emergency medical and specialist practices are a prime buyout target, because patients who need emergency care cannot haggle over price, and third-party payers guarantee payment. This satisfies the private equity business model of promising “outsized returns” to investors.

Private equity firms buy up small specialty physician practices that have begun to consolidate and “roll them up” into umbrella organizations to gain local, regional, and ultimately national market power. Researchers at the Kellogg School of Management found that most individual acquisitions were below the dollar threshold that would have required the transaction to be reported to antitrust regulators.

The new private equity–owned companies evade state laws that prohibit nonmedical ownership of doctors’ practices by setting up “physician management” or “management services” organizations, in which the physician group retains ownership of the practice itself and pays a fee to the private equity firm that owns the management company. But while doctors maintain autonomy over medical decisions, they also admit they are likely to be pressured to achieve higher patient volumes and revenues. They also give up any say over other management practices, such as the company’s billing practices.

In a typical contract, physicians receive a large up-front cash payment, which is calculated based on a multiple of the group’s EBITDA (earnings before interest, taxes, depreciation, and amortization) — with recent contracts reaching 12 times EBITDA. In addition, the doctors pay for an equity investment in the company by taking a large salary cut — up to 30 percent of their compensation. The payoff for the physicians is a “liquidity event” a few years later, with large payouts to the investors, including the doctors. The deal is particularly attractive to senior doctors who are nearing retirement, although that leaves the more junior doctors saddled with lower pay and greater uncertainty.

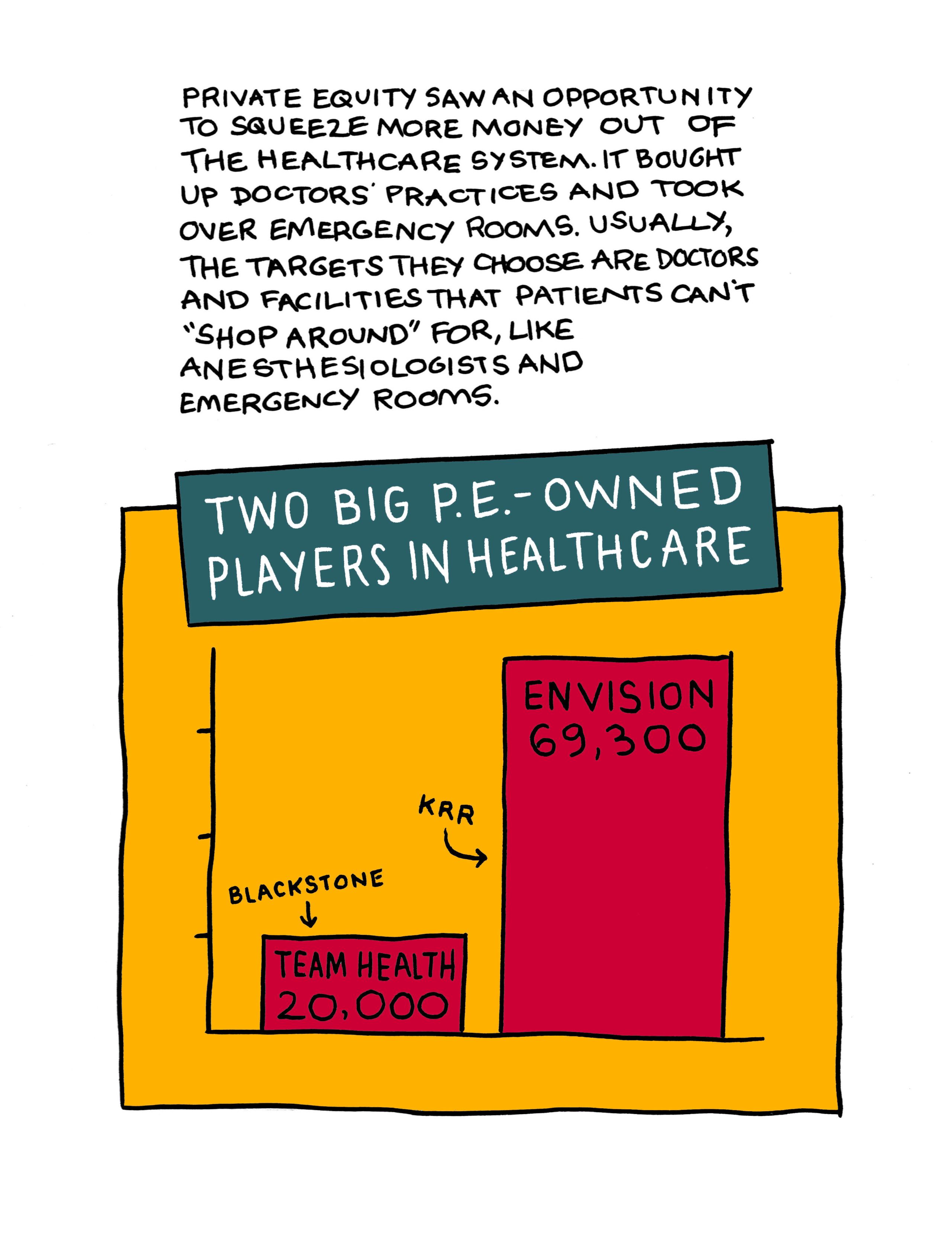

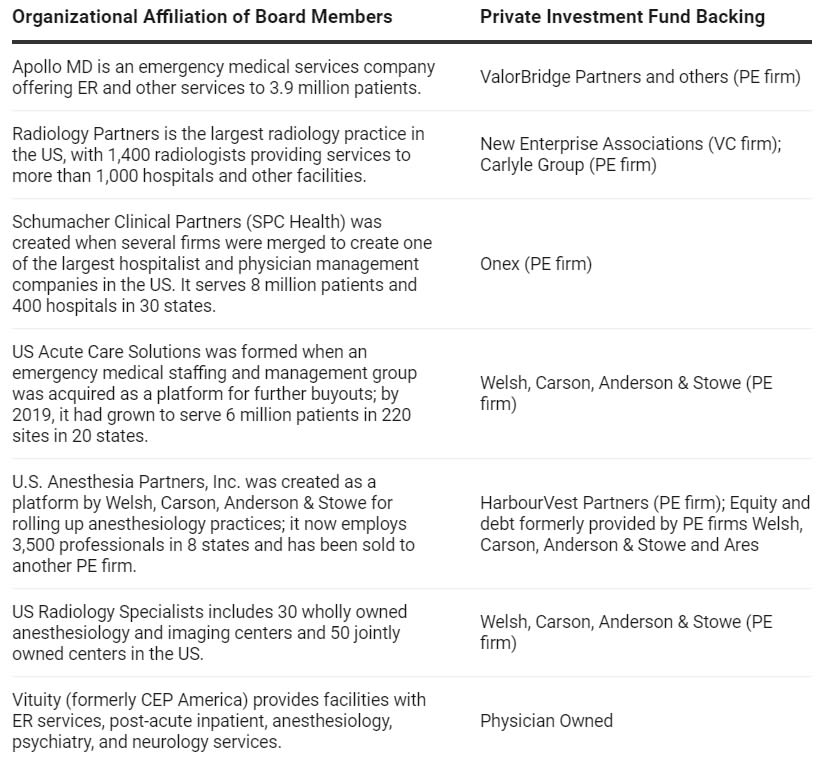

The Biggest in the Business

Private equity firms have accelerated buyouts of physician practices in the last decade. Leaders in this market include mega-PE companies Kohlberg Kravis Roberts (KKR) and the Blackstone Group, which own the two largest physician staffing firms in the country, Envision Healthcare and TeamHealth. These two firms have cornered 30 percent of the market for outsourced doctors, and collectively employ almost 80,000 health care professionals that staff hospitals and other facilities across the United States.

Envision Healthcare, formed in 2005, went private in October 2018 in a leveraged buyout to KKR. Its sprawling organization supplies doctors in 774 physician practices to hospitals and ambulatory surgical centers throughout the United States. Its emergency physician staffing company, EmCare Holdings, provides ER doctors, anesthesiologists, radiologists, hospitalists, and other specialists covering intensive care, medical, neonatal, pediatrics, psychiatric, skilled nursing, rehabilitation, and other inpatient units. Its outpatient ambulatory surgical arm (AMSURG) provides trauma and acute care general surgery in 260 facilities in 35 states.

TeamHealth was established in 1999 by a consortium of private equity firms as a platform for a physician staffing company. The Blackstone Group acquired it in 2005 in a leveraged (secondary) buyout. Blackstone returned TeamHealth to the public market in 2009 via an IPO, but then took it private again for $6.1 billion in February 2017. With passage of the Affordable Care Act in 2010, TeamHealth anticipated revenue growth via bundled payments and started buying up a series of ER and physician specialist practices — 51 companies between 2010 and 2016. It also bought IPC, a hospital management services company, allowing it to diversify across a wider range of care areas.

Two of the three air transport companies that together control two-thirds of this US market are private equity-owned Air Medical Group Holdings (AMGH) and Air Methods. KKR owns AMGH, a leading operator of medical helicopters, and merged it in 2017 with American Medical Response, the largest provider of ground ambulance services in the US. Air Methods, sold in 2017 to private equity firm American Securities, reported that it accounts for nearly 30 percent of total US air ambulance revenue. Its profit increased sevenfold from 2004 to 2014.

Our recent paper at the Institute for New Economic Thinking goes into more detail on these companies.

How Private Equity Drives Surprise Billing

Surprise billing has increased substantially because hospitals, under financial pressure to reduce overall costs, have turned to outsourcing expensive and critical services to third-party providers as a cost-reduction strategy. In an April 2019 survey, 41 percent of Americans reported they or a family member received an unexpected medical bill, with half of them attributing that bill to out-of-network charges.

Rates of surprise billing are highest among patients treated in an emergency room. In a review of 12.6 million ER visits by insured patients between 2010 and 2016, Stanford University researchers found that by 2016, 42.8 percent of all ER trips resulted in a surprise medical bill.

A team of Yale University health economists examined what happened when private equity–owned companies EmCare (part of Envision) and TeamHealth — the two largest emergency room outsourcing companies — took over the emergency departments at hospitals. An EmCare takeover translated into an 82 percent increase in charges for caring for patients. EmCare’s egregious surprise medical billing practices have resulted in a congressional investigation headed by former Missouri Senator Claire McCaskill, lawsuits from shareholders, and court actions involving Envision and UnitedHealth Group, the largest US insurer.

Blackstone’s TeamHealth has taken a different approach to billing that has nonetheless led to higher physician charges. It uses the threat of sending high out-of-network surprise bills for ER doctors’ services to an insurance company’s covered patients to gain high fees from the insurance companies as in-network doctors. TeamHealth emergency physicians typically would go out of network for a few months, then rejoin the network after bargaining for higher in-network payment rates — on average 68 percent higher than in-network rates received by the previous ER doctors. These practices contribute to higher health care costs — and ultimately higher insurance premiums for everyone — even if they do not directly lead to surprise medical bills. UnitedHealth, the nation’s largest insurance company, is pushing back on this by reducing TeamHealth’s higher in-network reimbursements by up to 50 percent.

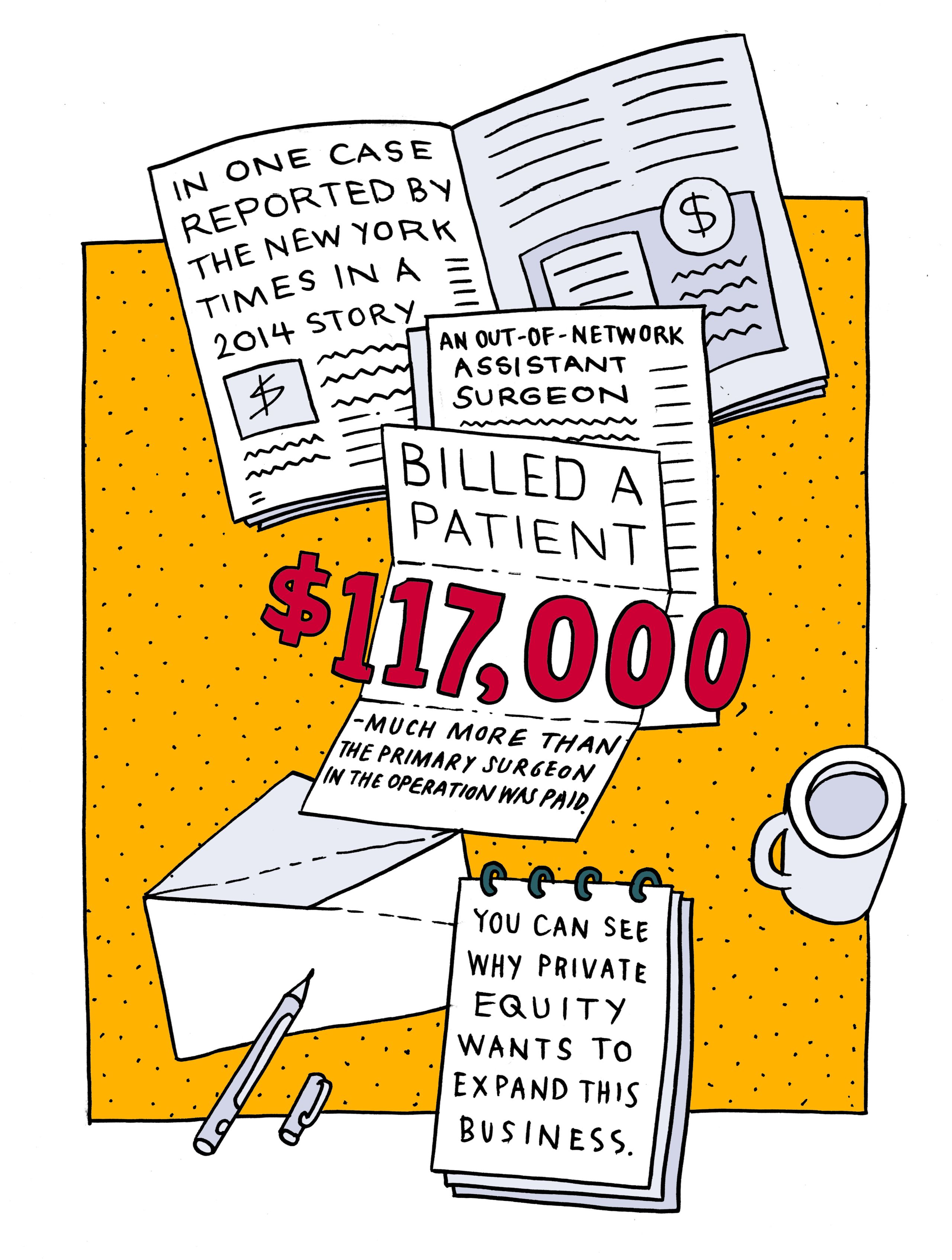

Patients in a hospital may encounter out-of-network physicians among ER doctors, specialties such as radiologists and anesthesiologists, assistants to a procedure, or hospitalists who check in on a patient. In a case that drew media attention, the patient’s own in-network surgeon billed $133,000 for his services, but accepted a fee of $6,200 negotiated with the insurance company. The out-of-network assistant surgeon, however, sent a bill for $117,000 and is seeking full payment of his charges.

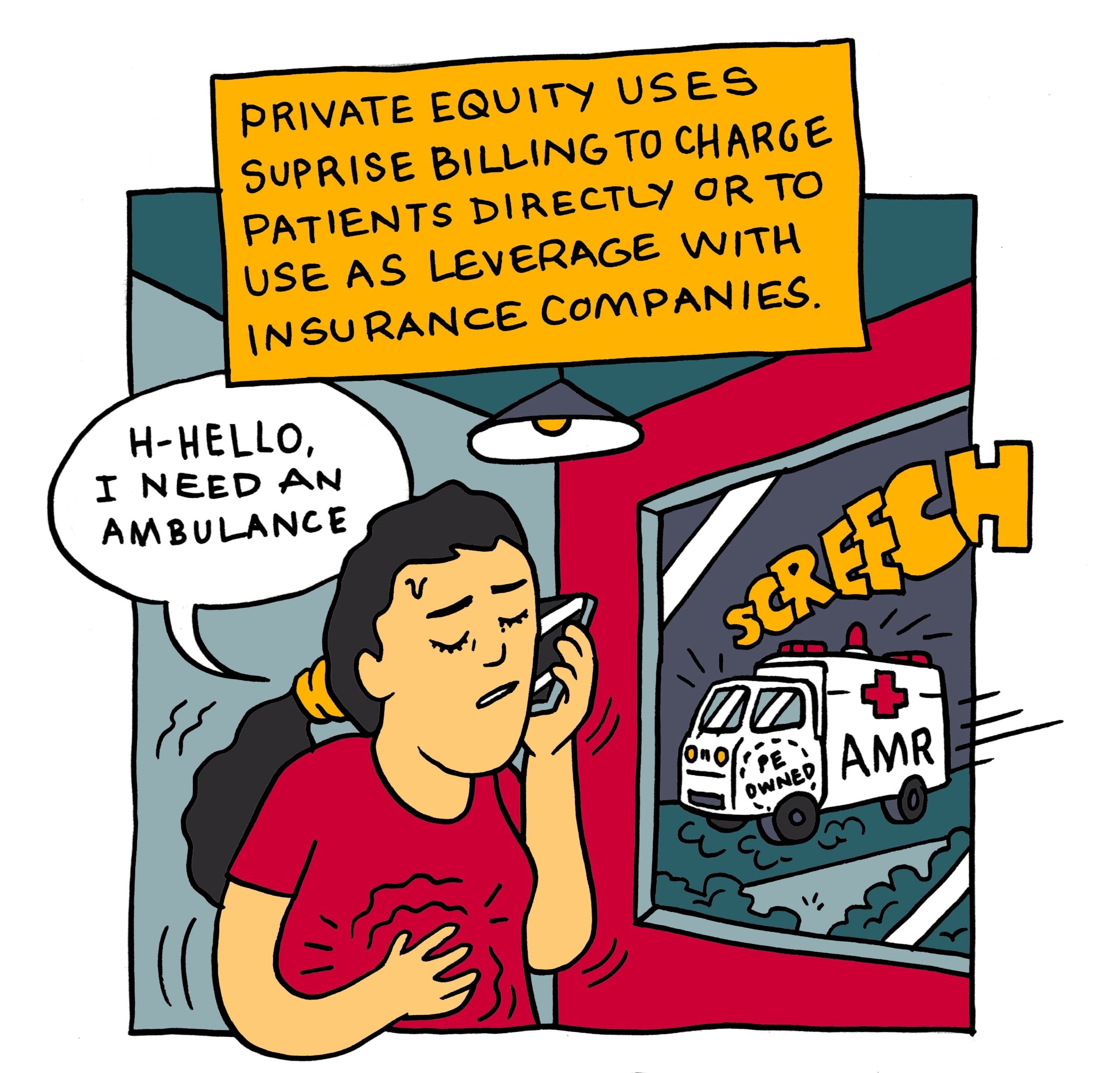

Surprise ambulance bills are even more common, occurring 86 percent of the time when an ambulance took a patient to the ER. A patient in an emergency situation who requires an ambulance to get medical help doesn’t get to choose the ambulance company. The result is another perfect opportunity for surprise medical bills, and a perfect target for unscrupulous investment funds.

In one study of air ambulance charges, Johns Hopkins University researchers found extremely large rate increases between 2012 and 2016. In 2016, these charges ranged from four to nine times higher than Medicare payments for air ambulance services. Some of the largest providers had among the highest charges. A 2019 study by the Government Accountability Office (GAO) found that the average cost of an air ambulance is over $36,000, and that 69 percent of the companies studied were out of network for the patient, who ended up being billed for most of the charge.

Surprise Billing: Illustrated

Let’s walk through an example of surprise billing.

1. You might be at home and think you have appendicitis. You call an ambulance because you can barely walk due to the pain. AMR — a private equity-owned ambulance service — is dispatched to get you.

2. You tell the ambulance to take you to the hospital that’s in-network for your insurance and has doctors you know. But you didn’t know that the ER was recently outsourced to a private equity-owned company that staffed it with out-of-network doctors.

3. You did have appendicitis! Your doctors decide to remove your appendix. Private equity is in the operating room too, although you wouldn’t know it. The surgeon’s assistant and the anesthesiologist are out-of-network, private equity doctors. The recovery room is no different: the substitute for the attending physician — the one who checks on you in your hospital bed — is a PE doc as well.

4. Once you’re at home and recovering one of two things can happen: you get surprised by bills from the ambulance, the ER doctor, the surgeon’s assistant, the anesthesiologist, and the attending doctor’s substitute...

OR

...the cost of these out-of-network providers is passed on to you via higher premiums.

But the net result is the same: for similar care, PE drives up costs in an already broken healthcare system.

Congress Steps In — and Private Equity Fights Back

More than three-quarters of Americans want the federal government to protect them from surprise medical bills, with 90 percent of Democrats, 75 percent of independents, and 60 percent of Republicans supporting federal legislation. While everyone — physicians, corporate staffing firms, hospitals, insurance companies, and patient advocates — purports to agree that insured patients should not be required to pay more than their plan requires for in-network doctors, questions remain about how proposed solutions will affect doctors’ pay, physician staffing firms’ revenues and profits, insurance company payouts, health care costs, and patients’ premiums.

At the beginning of the summer, it appeared that Congress would act to protect consumers from surprise medical bills, with the introduction in the Senate of the Lower Health Care Costs Act (S. 1895) by the Health, Education, Labor, and Pensions (HELP) Committee, and in the House, the No Surprises Act (H.R. 3630), by the House Energy and Commerce Committee. The main framework for these bills involves paying out-of-network doctors a rate “benchmarked” to rates negotiated with in-network doctors — the median in-network payment for this service or, alternatively, 125 percent of the Medicare payment.

Employers, patient advocates, and insurance companies favor this approach, which restricts how high an out-of-network doctor’s fee can go, restrains the growth of health care costs, and limits payouts that insurers can be made to pay. Major insurance companies and associations have formed the Coalition Against Surprise Medical Billing, which includes the American Benefits Council, America’s Health Insurance Plans, America’s Physician Groups, Blue Cross and Blue Shield, and the ERISA Industry Committee to lobby for benchmarking out-of-network doctors’ charges.

Not surprisingly, this solution is opposed by specialist physician practices, and by large physician staffing companies that want to continue to charge more than the in-network fees to patients. These companies, some backed by private equity firms, are lobbying intensively for a second option that would allow doctors to seek a fee higher than the benchmark via an arbitration process — in the belief that most settlements would ensure higher physician pay and higher company revenues and profits. Individual patients would no longer receive surprise medical bills, but arbitration awards would mean higher health care costs and would drive up premiums, deductibles, and co-pays for everyone.

Physicians for Fair Coverage, a private equity–backed group lobbying on behalf of large physician staffing firms, launched a $1.2 million national ad campaign in July to push for this second approach. Their argument is that insurance companies have created the problem of surprise medical bills by “forcing emergency room doctors, radiologists, anesthesiologists and other providers out of their networks.” The reality is that hospitals are outsourcing ERs, anesthesiology and radiology departments, and specialized care units to cut costs. Large physician staffing firms have positioned themselves to supply doctors to fill these positions or take over these units altogether.

Who is behind "Physicians for Fair Coverage"?

Data from PitchBook (accessed on August 28, 2019) and the book “Physician, Hospital Groups Gear Up for Fight on Surprise Medical Bills” by Susannah Luthi.

Data from PitchBook (accessed on August 28, 2019) and the book “Physician, Hospital Groups Gear Up for Fight on Surprise Medical Bills” by Susannah Luthi.

The opposing camps lobbied for their positions over the summer, as seen in the jockeying over the House Energy and Commerce Committee’s No Surprises Act. It was supported by Committee Chair Frank Pallone (D-NJ) and ranking member Greg Walden (R-OR) and would have benchmarked fees paid to out-of-network doctors to the negotiated rates paid to in-network providers. But in July, Representatives Raul Ruiz (D-CA) and Phil Roe (R-TN) introduced the arbitration amendment, amid intense lobbying from large corporate and investor-owned physician staffing firms.

Pallone and Walden accepted the amendment because it allowed arbitration only in special cases, and required the arbitrator to use negotiated rates — not provider charges — when deciding on disputes over payment. Supporters of the original bill were unhappy. As Loren Adler, associate director of the USC-Brookings Schaeffer Initiative for Health Policy, noted, the amendment is a giveaway to private equity interests that will have adverse effects on patients, employers, and taxpayers — even if the arbitration option’s limited scope would limit potential harm. As the bills move forward, compromise on including limited use of arbitration panels in the legislation may be necessary in order to win passage.

Wall Street analysts have been closely monitoring these debates, given the substantial debt funding that private equity firms rely on to create large physician staffing firms, such as KKR’s Envision Healthcare. Investors fear that any congressional deal that limits what out-of-network doctors are paid will seriously jeopardize Envision’s business model, which relies on collecting excessive fees from unsuspecting patients who are hit with surprise medical bills. Envision’s creditors are concerned that without the ability to charge these high fees, the company will have difficulty repaying the debt it took on as part of the financing when KKR bought it out for $9.9 billion in 2018. The value of Envision’s $5.4 billion loan due in 2025 tumbled to 87.8 cents on the dollar at the end of July 2019 and to 77.3 cents by the end of August. As Envision’s creditors are well aware, the company’s solvency and KKR’s returns are threatened by legislation that protects patients.

By midsummer, an aggressive “dark money” campaign emerged that many believe is intended to derail any legislation. In July and August, Smart Media Group subsidiary Del Cielo Media poured $13 million into TV, social media, and radio ads on behalf of a mystery group, Doctor Patient Unity, in the home districts of 13 Republican and Democratic senators who are up for re-election. The ads oppose any limits on what doctors can charge and accuse insurance companies of not wanting to pay their fair share of doctors’ fees.

Congressional staff are concerned that the big-money displays will intimidate legislators who may fear even larger expenditures to unseat them if they support any of the legislative proposals under consideration. This could thwart the passage of consumer protection measures altogether, leaving patients on the hook for large, unexpected medical bills — a continuation of current practices that have enriched PE-backed and other corporate physician staffing and management services firms.

The debate over surprise medical bills has been framed as doctors who only want to be paid for their lifesaving services and insurance companies that don’t want to pay them fairly. Viewed that way, it’s a debate that insurance companies are sure to lose. But these are not the true protagonists. Private equity firms are buying up specialty doctors’ practices at an alarming rate because surprise medical bills allow them to extract high payments for medical care from patients and/or insurance companies. It’s private equity whose interests are opposed to those of insurance companies. And insurance companies which, in defending themselves against exorbitant payments to these doctors, are also acting to hold down health care costs and health insurance premiums for consumers.

Now, even as compromise bills appear ready to advance, the question is whether politicians will stand up to the multimillion-dollar dark-money campaign launched in the summer. Will intense negative lobbying scuttle attempts to rein in surprise billing? Patients hit with these bills will be the biggest losers, but everyone will lose as health care costs and insurance premiums rise. Whoever is behind this campaign, private equity firms like Blackstone, KKR, and Welsh, Carson, Anderson & Stowe will be the big winners. PE’s role is hidden from view, and the campaign may well succeed in diverting blame for unexpected and outrageous charges to the insurance companies.

If you appreciated this work, please consider a donation to support the Center for Economic and Policy Research.

Eileen Appelbaum is Co-Director at the Center for Economic and Policy Research. This article draws on her book with Rosemary Batt, Private Equity at Work: When Wall Street Manages Main Street.

Rosemary Batt is the Alice Hanson Cook Professor of Women and Work at the Industrial and Labor Relations School, Cornell University.

Artwork by Sam Wallman.

This project was supported by the Institute for New Economic Thinking (INET) and the Laura and John Arnold Foundation.

A version of this article appears in The American Prospect, Prospect.org, Fall 2019. Used with permission.